Market Commentary – March 2016

The S&P ASX 200 has fallen 4% in another volatile quarter. The market fell heavily from the New Year high with the ASX 200 falling 8% in January and recovering slowly in February and March. The major financial themes impacting the Australian market continue to be:

- The price of commodities – have improved marginally after extraordinary falls

- Chinese economic transition – China has indicated it currently favours reform over growth

- Australian economic transition – The RBA is satisfied the economy continues to rebalance after the mining boom

- US interest rates – The FED has taken a less aggressive approach to increasing interest rates reverting to a wait and see approach

We believe these trends will remain for the foreseeable future and we believe caution is warranted with current market outlook and a distinct lack of growth drivers for the economy.

Australia

- The Reserve Bank of Australia (RBA) kept the cash rate at 2% p.a. stating “there are reasonable prospects for continued growth in the economy, with inflation close to target”.

- The labour market on the Eastern Seaboard continues to improve with the unemployment rate falling to 5.8%.

- Wage growth remains soft and below long term average

- Sydney and Melbourne housing markets recent strong returns have ended and prices have moderated

- The Australian dollar rose against the USD closing in March above $0.76 USDs.

- The headline inflation rate has crept up from 1.5% to 1.7% but remains below the RBA target range of 2-3% pa leaving scope to further cut interest rates in order to stimulate the economy should the support be required.

- The Prime Minister Malcolm Turnbull’s honeymoon period appears to have ended abruptly with a budget due on the 3rd of May and talk of an early Election in July

US

- The US S&P 500 and Dow Jones Industrial Average recovered increasing 2.3% and 1.5% respectively following steep declines in January

- The US FED (Federal Reserve System – The US Central Bank) have left interest rates on hold at 0.5% taking a wait and see approach to further interest rate increases

- The US economy continues to strengthen with:

- Growth has eased but remains positive

- Household consumption above average

- Increasing employment

- Stable inflation

- Still no wage growth

- US presidential election campaigns have begun for the November 8, 2016 Election. Currently candidates are vying for party nominations at this stage Trump vs Clinton seems the most likely outcome

Europe

- European economy continues to struggle and growth remains illusive

- Terrorism remains a key theme in European markets with recent attacks in France and Belgium. Interestingly sharemarkets seem to be more desensitised to their occurrence

- Greece continues to have issues but the rest of the world has largely moved on

- Russian political issues have been overshadowed

- Political situation in Europe is currently far worse than Australia with

- UK voting on whether to stay in the Euro Zone

- Spain unable to form a Government

- France the far right party of le National Front is gaining momentum

- The European mood can be summed up as:

- Anti-Austerity

- Anti-American

- Anti-Euro

- Anti-Immigration

China

- The Chinese Economy has a new 5 year plan which favours growth over economic rebalancing all be it at lower target of 6%

- A developing property issue where house prices in some cities are raising strongly while others fall dramatically

- China is experiencing a capital flight as more and more Chinese find ways to move their wealth off-shore to escape devaluation of the Yuan and evade capital controls

- This poses a problem as China has a fixed currency and as citizen move their money out the Peoples Bank of China must drain their reserves to replace the money in order to maintain the fixed exchange rate

Looking Ahead

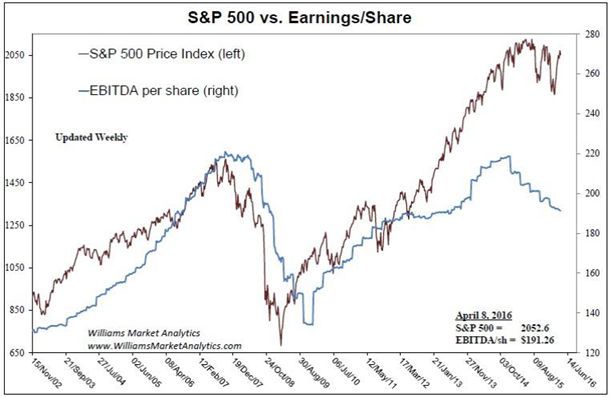

We believe the Chinese and US sharemarkets remain expensive. The US sharemarket earnings season for the fourth quarter was average and earning are predicted to decline in the next earnings season. The graph highlights our concern regarding markets. It shows a growing disparity between prices and company earnings of companies listed on the S&P500. This could be a catalyst for share market correction.

The events that will impact the market this year are likely to derive from politics and currency valuations. The currencies will be the falling Chinese Renminbi and the raising US Dollar. The major political events this year are the US Presidential Election in November and an Australian Election is expected be called late July 2016. June 23 will see the UK vote on “Brexit” which is likely to cause volatility in Europe and a weakening of the pound. With respect to China we believe stability issues are political in nature with the Chinese leadership attempting to root out significant corruption and shore up their leadership.