The Australian Sharemarket rose strongly in the March quarter. The S&P ASX200 closed at 5,891. The strong performance was driven by the continued search for yield. Magnified by a 0.25% pa cut in the Reserve Banks interest rate and market expectations of further interest rate cuts. Creating fear in the fixed interest market as deposits mature with investors looking to replace relatively safe high yield returns.

Australia

- The Reserve Bank of Australia (RBA) cut the cash rate 0.25% to 2.25% pa at the February meeting in order to provide “additional support to demand”

- The labour market remains soft with unemployment continuing to increase and low wages growth persisting which will effect consumer confidence and spending in the coming months

- Lowering the interest rate has proved a boon to Sydney and Melbourne housing markets however, house prices have struggled in other major cities

- The Australian dollar continued its decline closing at $0.78 USDs however the RBA considers this to be above most estimates of its fundamental value particularly when the significant decline in commodity prices is taken into account

- The inflation rate has fallen below the RBA target range of 2-3% currently 1.7% pa giving room for further interest rate cuts

- The RBA continues to entice the market with the possibility of rate cuts in the future

US

- The US S&P 500 and Dow Jones Industrial Average finished the period flat on concerns of when the FED would begin to lift interest rates

- The US economy continues to strengthen

- FED Chair Janet Yellen remains dovish or biased towards waiting for clear evidence that a rate raise is needed to cool the US Economy

Europe

- European economy continues struggle

- The Greek General Election was won by the left-wing Syriza party lead by Alexis Tsipras. This has led to ongoing negotiations between Greece and EU Member Nations. At this stage it seems that Greece is winning the “Grexit” battle by altering the conditions of previous bailout agreements to be more accommodating for Greece

- The Ukraine/Russian dispute continues. However, the dispute has not been making headlines with Europe currently largely focusing on Greece

China

- Growth of the Chinese economy continues to slow

- The concern of a property bubble in China grows

- The People’s Bank of China (POBC – RBA equivalent) is attempting to manage economic growth though cutting interest rates and using macro prudential (policy) tools to control the property markets

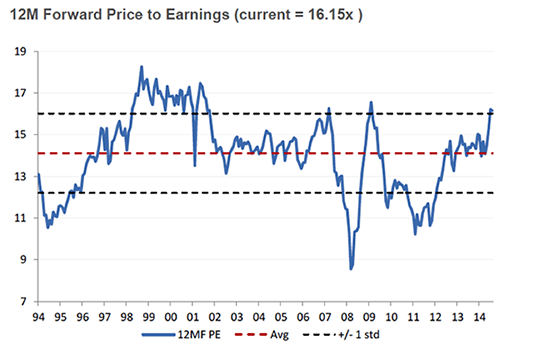

We have seen the Sharemarket recover somewhat dramatically, however the recovery is not based on sound principals, but the necessity to generate a specified yield. The below graph shows the overall market Price to Earnings since 1994. This implies that on average the market is becoming expensive. The elevated valuations of companies has provided the opportunity to build portfolio cash.

Should you have any queries or want to discuss the above or your portfolios please do not hesitate to contact us.